The latest issue of SCORViews, the newsletter of SCOR Global Life in the Americas, features articles written by senior managers and analysts who examine emerging trends and important tactical issues in the life insurance industry. This October 2017 publication focuses on a study led by SCOR to deepen clients’ understanding of their mortality experience.

Broad based industry studies demonstrate general mortality trends, but shed little light on how an individual company’s experience compares to its peer group. To deepen clients’ understanding of their mortality experience, SCOR conducted a comprehensive study that offers participants a view of their experience against all study participants (aggregate study) as well as a select group of peers (peer group study). In the future, we look forward to possibility expanding the number of participating companies beyond those included in this initial study.

A total of 18 companies participated in our first SMI study. Analysis focused on traditional, fully underwritten business. The study covered years 2010-2014 and issue years 1995 and later in order to capture modern preferred underwriting classes popular in the market. Face amounts $50K and greater for Permanent (Perm) products and $100K and greater for Term products were also included. In general, these face amounts have similar underwriting and distribution methods. The study excluded conversions, COLI/BOLI business and SI/GI underwritten products.

Overall results of the study are below, using the 2015 VBT RR100 (2015 VBT) industry mortality table as the expected basis.

Key Insights from the Aggregate Study

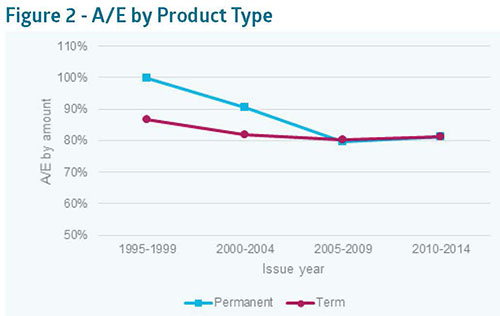

Product Type – Perm products appear to experience higher A/Es than Term products. This is primarily driven by older policies issued when underwriting was not split out into today’s preferred class structure.

Compared to Term, the issue year eras where Perm products are more heavily weighted to standard risk classes have A/Es that are higher than Term. For the issue year eras where Perm and Term products have similar exposure to preferred risk classes, they also have similar A/Es by amount. This is consistent with anti-selection that was observed in the market as Perm products lagged behind Term in the introduction of preferred class structures.

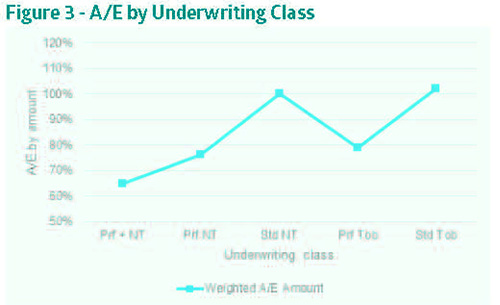

Underwriting Class – The mapped underwriting class structure produces results where mortality improves with better risk classes. While preferred classes are broken out into ‘Prf+ NT’ and ‘Prf NT’, the standard class broke into standard plus and residual standard more recently. Due to lower credibility in standard classes, both are grouped into ‘Std NT’.

Due to company-specific differences in underwriting requirements and thresholds, a considerable spread exists around this overall average. The above results provide ‘rules of thumb’ to inform a high level benchmark for reasonable levels of mortality by class but vary by company.

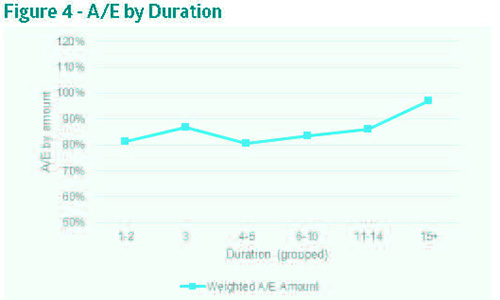

Duration – While the 2015 VBT does not remove contestable claims from the first two durations, a bump in duration 3 A/Es by amount continues to exist in the experience.

Due to the construction of the 2015 VBT, lower A/Es in durations 1-2 are not expected. The study confirms this with durations 1-2 and 4-5 having similar A/E ratios, both of which are close to the overall A/Es of more recent issue year business overall. The higher A/E in duration 3 indicates an increase from what is expected in the VBT table. Experience after the contestable period ends varies among companies based on each company’s claims contesting policies and success rate.

The generally increasing trend by duration is partially due to the older issue years contributing to later durations. Where earlier issue years with less preferred business have higher A/Es, they also drive later duration experience higher.

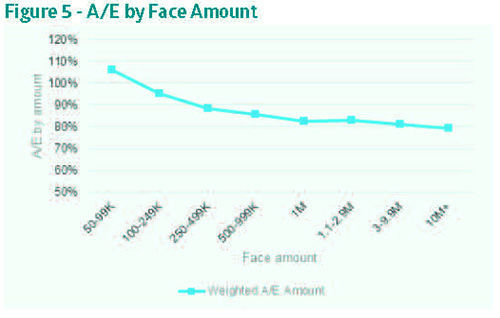

Face Amount – A commonly observed pattern in mortality studies is improving experience as the face amount of policies increase. This downward trend substantiates the value of additional underwriting evidence required at larger face amounts and of socioeconomic factors that contribute to better mortality. More affluent policyholders tend to have better access to health care, healthier lifestyle choices and less exposure to certain hazards. This pattern is observed in the overall study up to and including policies at $1M. Thereafter, in face amounts greater than $1M, experience stabilizes and continued improvement is less apparent.

The study results did not evidence deterioration in mortality at the highest face amounts above $10M. While high-risk behavior in the most affluent has been thought to create a ‘mortality smirk’, or uptick, results at these high face amounts did not support this hypothesis, though the analysis is based on a limited number of claims.

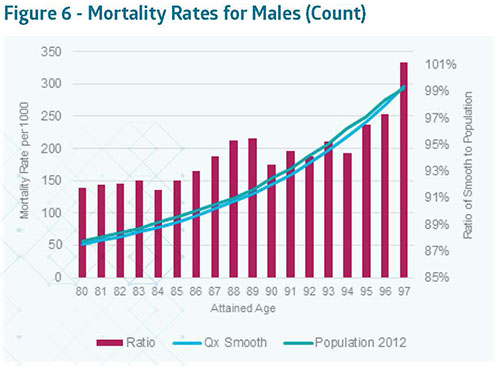

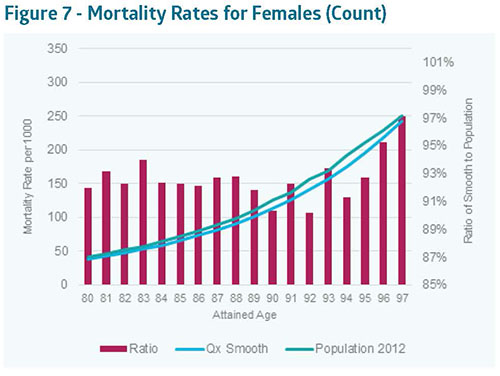

Attained Ages 80+ – Mortality begins to grade to population mortality at attained ages in the mid- to high-90s as underwriting selection and market forces have worn off.

As shown in Figures 6 and 7, older attained age mortality rates from the aggregate study range from about 90% to 95% of population rates for both male and female and begin to grade to 100% at the older ages. At these super high ages, mortality should begin to approach population. Underwriting has generally worn off and these super-seniors would be the very healthiest in the population (or else they would not have survived to these ages). Any selection effects from initial underwriting or market forces should have almost completely worn off.

Through SMI, we value the opportunity to partner with our clients to analyze mortality in an innovative way. We hope that by doing so we collectively deepen our understanding of developing mortality trends and their contribution to strategic decision making.

Author:

Katherine Warner, FSA, MAAA

Assistant Vice President, Marketing Actuary - R&D