What should we make of European insurers' Solvency II disclosures?

Interaction between financial information and the reinsurance underwriting process.

18 avril 2018

In this Technical Newsletter, Laurent Rousseau, Deputy Chief Executive Officer of SCOR Global P&C, focuses on the impact for insurers of greater public disclosures, looking at the value of the disclosed information for reinsurers and the advantages in terms of better understanding client needs and implementing the most appropriate solutions.

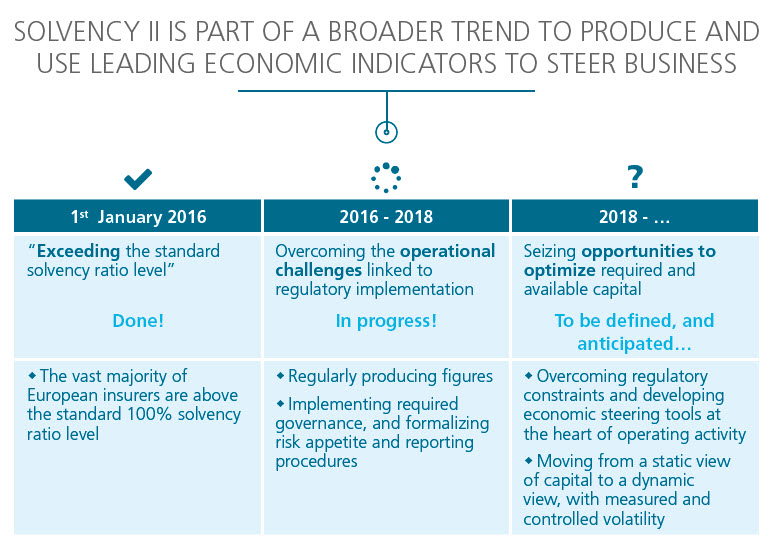

Solvency II regulation has been in force for over 2 years. Its effects have yet to be fully felt by insurance companies, customers, regulators, and capital providers. However, we already see a number of impacts well beyond the regulatory solvency framework.

Considering Solvency II in a broader sense than its strict regulatory nature, we begin to see how:

- Pillar I provides the tools for capital management sophistication and optimization;

- Pillar II provides a framework for better risk appetite setting and governance in general;

- Pillar III should be an integral part of a risk management and financial communications strategy.

The consequences of Pillar III are familiar to insurers already using capital markets for their debt and equity funding. Many other insurers, especially mutuals, are not used to so much transparency, plus the constraints and long-term consequences that go with it. Nevertheless, over time, Solvency II and the disclosures required by Pillar III should catalyze greater sophistication in the management of risk and capital among all insurers.